All Categories

Featured

Table of Contents

Comparable to various other life insurance coverage plans, if your clients smoke, use other types of tobacco or nicotine, have pre-existing wellness conditions, or are male, they'll likely need to pay a higher price for a last cost policy (final burial expenses). The older your customer is, the greater their rate for a plan will be, since insurance coverage firms think they're taking on more threat when they use to insure older clients.

The plan will likewise remain in pressure as long as the insurance policy holder pays their costs(s). While numerous various other life insurance coverage policies may call for clinical tests, parameds, and attending physician statements (APSs), final cost insurance coverage plans do not.

Final Expense Selling

Simply put, there's little to no underwriting needed! That being stated, there are two main types of underwriting for final cost strategies: streamlined problem and guaranteed problem. end of life insurance plans. With streamlined problem strategies, clients typically only need to respond to a few medical-related inquiries and may be refuted insurance coverage by the carrier based on those responses

For one, this can enable agents to determine what kind of plan underwriting would function best for a specific client. And two, it assists representatives narrow down their client's options. Some carriers may invalidate customers for protection based upon what medications they're taking and for how long or why they've been taking them (i.e., maintenance or treatment).

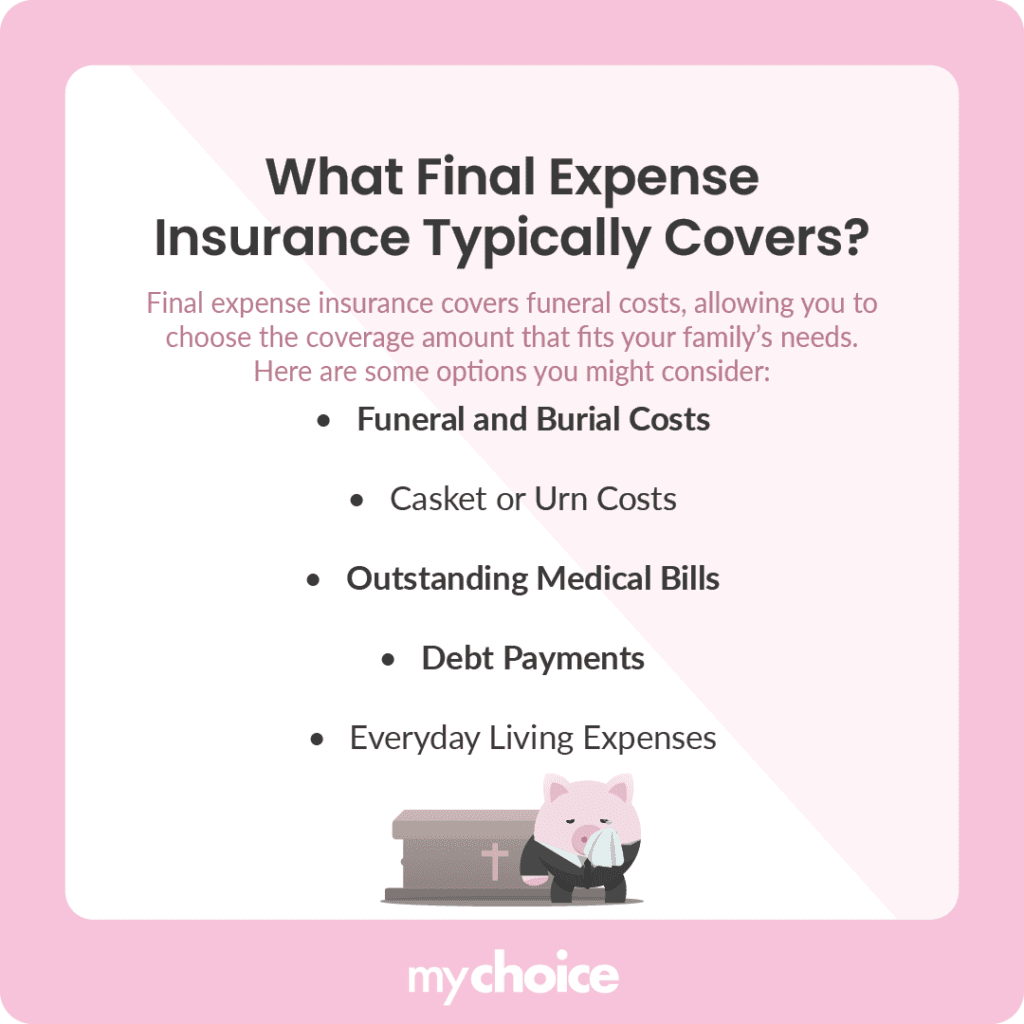

Insurance To Cover Funeral Expenses

The short response is no. A last cost life insurance policy is a sort of irreversible life insurance policy. This means you're covered up until you die, as long as you've paid all your premiums. While this policy is created to aid your recipient pay for end-of-life expenditures, they are complimentary to use the death benefit for anything they need.

Similar to any type of other long-term life policy, you'll pay a regular premium for a final expense policy in exchange for an agreed-upon fatality advantage at the end of your life. Each provider has different rules and alternatives, however it's relatively easy to handle as your recipients will certainly have a clear understanding of just how to spend the cash.

You may not require this type of life insurance policy (final expense insurance florida). If you have long-term life insurance policy in place your final costs might currently be covered. And, if you have a term life plan, you may be able to transform it to a long-term policy without a few of the added steps of getting final cost coverage

Funeral Insurance Brokers

Developed to cover minimal insurance coverage needs, this kind of insurance can be a cost effective alternative for individuals who simply wish to cover funeral expenses. Some policies may have limitations, so it is essential to review the small print to ensure the policy fits your requirement. Yes, certainly. If you're trying to find an irreversible choice, universal life (UL) insurance remains in location for your whole life, so long as you pay your premiums.

This option to final expenditure insurance coverage provides alternatives for extra family protection when you need it and a smaller protection amount when you're older. budget funeral cover.

5 Essential facts to remember Planning for end of life is never ever positive. Neither is the idea of leaving liked ones with unforeseen costs or financial debts after you're gone. Oftentimes, these monetary obligations can stand up the settling of your estate. Consider these 5 truths regarding final expenditures and just how life insurance coverage can assist pay for them - burial covers.

{kind=link}

Latest Posts

Final Expense Insurance Vs. Life Insurance

Better Life Funeral Policy

Get Funeral Insurance